Business

Launch of Apple Card is Imminent: Here’s What You Need to Know

The New Offering Will Take Off Fast, Based on the Perks and Details…

As with most things financial, there are lots of details, but some interesting perks, particularly for frequent customers of Apple products.

Immediate sign up on your iPhone

First perk: no lengthily complicated application process. According to the pre-launch information (see video above), just go to the Wallet app and tap on the Apple Card interface (once the Card is live) and go through the simple activation steps.

Once the sign up steps are complete, you can immediately start using the card as you would Apple Pay.

Small but expected caveat: For non-Apple Pay purchases in a traditional store setting you will need to wait until your physical card arrives in the mail. Also, although a pre-approved status will often be in place, availability is still subject to qualification, like any credit card.

Using the Card

The card will function as would any other card in your wallet for Apple Pay. This includes online purchases and in-store checkout where you normally would use Apple Pay.

You can designate the Apple Card as your default payment method in your wallet for purchases using your iPhone, iPad, Mac or Apple Watch.

The MasterCard Goldman Sachs Connection

The extended uses for the digital and physical version of the card are enabled through the partnership between MasterCard and Apple. You will be able to use the Apple Card anywhere that a MasterCard is accepted.

Goldman Sachs is the credit provider for your Apple Card and they will set your interest rate based, as would be expected, on your current credit score. Rates are projected to be in the range of 13.24% to 24.24% which is below the average in the US.

An extended fixed payment system is likely to be offered for large purchases according to the pre-release data.

Main Perks and Advantages

There are many unconventional and improved aspects to the use and especially the user experience associated with the new card. In the keynote announcement earlier this year (see video above) a great emphasis was made on the ways that the project was focused on improving the experience and helping users attain a healthier financial lifestyle.

This includes various features designed to help reduce interest charges, not only by offering lower overall rates, but by giving the user options and calculations that can provide payment alternatives to the traditional “minimum monthly” payment currently the norm.

Payments can be made from your linked bank account or can be transferred from Apple Cash in your Wallet app.

There is no annual fee for the card, no international fees and no fee for exceeding your credit limit or making a late payment. Also, there is not increased interest rate penalty, per se, for late payment, which is common in some other credit card accounts. Late payment will, naturally, result in interest accrual, but based on your current rate.

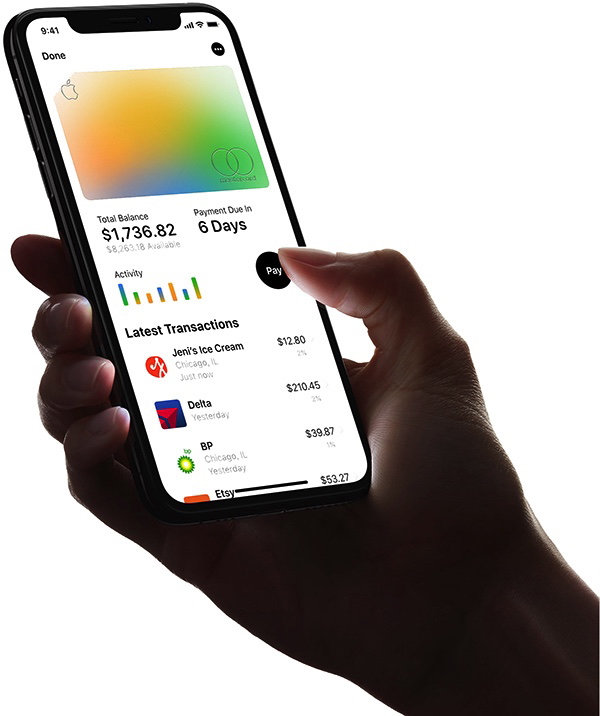

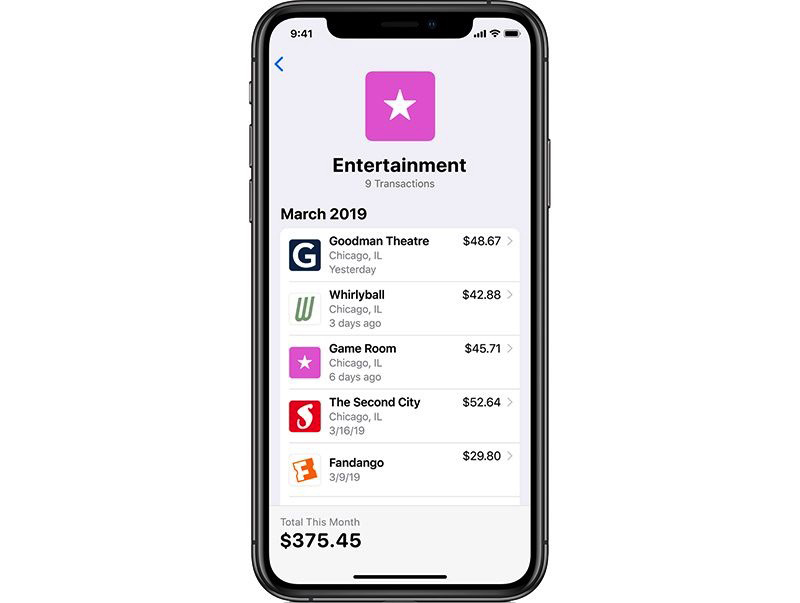

There is an separate app, particularly useful on iPad, which does not have the Wallet app, where data on transactions, payments and other details are provided. This, in typical Apple style, is far superior to any credit card app interface from banks and lenders.

Rewards and “Daily Cash”

Rather than a points system commonly seen on traditional credit card accounts, the Apple Card has a cash back system which can kick back up to 3% on a daily basis.

They call this “Daily Cash” and, as the name implies, your rebated cash will be credited to your account every 24 hours and be directly transferred to your Apple Cash account. If you do not sign up for Apple Cash, you will get your rebates sent to your bank account monthly.

Percentages vary, 3% is for all purchases made directly from Apple, 2% for all Apple Pay transactions and 1% for using the physical card at any non-Apple Pay retailer.

There is no cost to transfer your rewards cash to your bank account and this can take from one to three days. There will be an option to get instant transfers, which will incur a 1% fee. The transfers are done through the Apple Cash card from the Wallet app to the linked bank account.

Best Features and Conclusion

The overall sense is that this is going to be a very popular offering, based on the positive attributes of the card and the deal.

Although the terms are clearly slanted towards encouraging financial activity benefiting the emerging Apple financial eco-system, with the reward percentage on direct Apple purchases and Apple Pay coming in higher than the “out of network” transactions made with the physical card only, the rest of the perks are more than enough to pique the interest of a great number of iPhone users.

The titanium card appearance, styling and feel will attract many for that reason alone. Quel chic! And it is likely that the card will cause an increase in Apple Pay transactions, with double cash back for pulling out your iPhone instead of the physical card.

Ultimately, the software tools enabling privacy – no data to Apple and Goldman Sachs promising never to use or sell your data – along with the fantastic tools for tracking transactions, spend, payments and interest are perhaps the most likely to create love.

Who doesn’t hate dealing with credit card companies and their antiquated interfaces and systems? Some credit card providers do not even allow automatic payment scheduling, apparently hoping you will pay late so they can rack up those late payment penalty fees. Doing away with even the worst, most evil, aspects of credit card accounts is already a huge step forward.

Let’s hope that Apple will manage this as well as it appears. It looks like a top flight offering that has plenty of advantages that make it head and shoulders above the pack, and, for iPhone users it seems like a “must have” if there ever was one.

- Easy sign-up on iPhone

- Accepted worldwide (wherever Mastercard is available)

- Up to 3% cash back

- Daily cash back

- No fees

- Engraved Titanium physical card with concealed numbers

- Spending tracking

- Clear transaction labeling with more data

- Built-in Privacy

Find books on Big Tech, Sustainable Energy, Economics and many other topics at our sister site: Cherrybooks on Bookshop.org

Enjoy Lynxotic at Apple News on your iPhone, iPad or Mac and subscribe to our newsletter.

Lynxotic may receive a small commission based on any purchases made by following links from this page.