New Zealand officials on Thursday heralded passage of a groundbreaking law requiring financial institutions to disclose climate-related risks.

“This is a landmark day,” Commerce and Consumer Affairs Minister David Clark said in a speech to Parliament.

At issue is the Financial Sector (Climate-related Disclosures and Other Matters) Amendment Bill, which had its third reading Thursday.

A summary of the measure from the Business Ministry touts the bill as a step toward making the country’s “financial system more resilient” and reaching New Zealand’s goal of net zero CO2 emissions by 2050. According to the ministry, the goals of the bill are to:

ensure that the effects of climate change are routinely considered in business, investment, lending, and insurance underwriting decisions;

help climate reporting entities better demonstrate responsibility and foresight in their consideration of climate issues; and

lead to more efficient allocation of capital, and help smooth the transition to a more sustainable, low emissions economy.

A joint statement Thursday from Clark and Climate Change Minister James Shaw frames the bill, which will require the annual disclosures starting in 2023, as the first of its kind across the globe.

“This bill will require around 200 of the largest financial market participants in New Zealand to disclose clear, comparable, and consistent information about the risks, and opportunities, climate change presents to their business,” Clark said in the statement. “In doing so, it will promote business certainty, raise expectations, accelerate progress and create a level playing field.”

Shaw, for his part, said the measure would “encourage entities to become more sustainable by factoring the short, medium, and long-term effects of climate change into their business decisions.”

“New Zealand is a world-leader in this area and the first country in the world to introduce mandatory climate-related reporting for the financial sector,” added Shaw. “We have an opportunity to pave the way for other countries to make climate-related disclosures mandatory.”

Originally published on Common Dreams by ANDREA GERMANOS and republished under a Creative Commons License (CC BY-NC-ND 3.0).

The number of multimillion-dollar individual retirement accounts has soared in the past decade, as more wealthy Americans use the tax-advantaged vehicles to shield fortunes from income taxes, according to new data released by Congress today.

The data reveals for the first time the staggering amount of money socked away in tax-free mega Roth accounts: more than $15 billion held by just 156 Americans.

The new data also shows that the number of Americans with traditional and Roth IRAs worth over $5 million tripled, to more than 28,000, between 2011 and 2019.

The data was requested by Senate Finance Chairman Ron Wyden, D-Ore., and House Ways and Means Chairman Richard Neal, D-Mass., following ProPublica’s story last month exploring the rise of mega Roth IRAs. The story, based on confidential IRS data obtained by ProPublica, revealed that tech mogul Peter Thiel has the largest known Roth IRA, worth $5 billion as of 2019.

In a Senate Finance hearing on retirement on Wednesday, Wyden said such massive accounts underscore the country’s inequalities. “Individuals at the very top — at the very, very top — are able to game the rules to get ahead and basically abuse taxpayer-subsidized accounts with pricey accountants and lawyers,” Wyden said. “This increases the already existing retirement inequality between retirement haves and have-nots to an extreme level.”

Roth IRAs were established in 1997 to incentivize middle-class Americans to save for retirement. Congress imposed strict limits, including a cap on how much can be contributed to the accounts each year, which today stands at $6,000 for most Americans. The average Roth account was worth $39,108 at the end of 2018.

But a select set of the ultrawealthy have managed to get around limits set by Congress and transformed the vehicle into a powerful onshore tax shelter. One way they’ve done that is by buying nonpublic shares of companies with extremely low valuations. That allows them to tuck a huge volume of shares into a retirement account. Congressional investigators have previously found that the IRS has struggled to enforce rules around these investments, including whether the valuations are legitimate.

Once money is deposited into a Roth account, any proceeds from investment gains are tax free. So, for example, a Roth owner who sells a successful tech investment for a $1 million profit gets to keep all of the money, saving a potential $200,000 in federal taxes. The savings can then be reinvested, tax free, as long as the Roth holder waits till he or she is at least 59 and a half before withdrawing the money. Owners of traditional IRAs, by contrast, enjoy tax-free growth but must pay income tax on withdrawals. The Roth is considered the more powerful tax-avoidance tool for the wealthy.

The latest numbers come from analysts at Congress’ nonpartisan Joint Committee on Taxation. They update a widely cited study from the Government Accountability Office that released figures on large IRAs in 2011.

The new figures show that, as of 2019, nearly 3,000 taxpayers held Roth IRAs worth at least $5 million. (The total of more than 28,000 people holding IRAs of that size includes both traditional and Roth IRAs.) The aggregate value of those Roth IRAs was more than $40 billion.

Both Wyden and Neal said in statements that the new figures show the need for reform. Neal said that “IRAs are intended to help Americans achieve long-term financial security, not to enable those who already have extraordinary wealth to avoid paying their fair share in taxes and deepen existing inequalities in our nation.” Neal said earlier this month, in the wake of the ProPublica article, that the Ways and Means Committee would draft a bill to “stop IRAs from being exploited.”

For his part, Wyden said, “As the Finance Committee continues to develop proposals to make the tax code more fair, closing these loopholes will be a top priority.” Wyden first proposed an overhaul of IRA rules to prevent the accounts from being used as large tax shelters several years ago. One reform that is being discussed would prohibit investors from putting assets that are not available to ordinary Americans, such as shares of startup companies, into retirement accounts.

Wyden and Neal’s push for reforms comes as Congress is considering bipartisan retirement legislation. The bills are being pitched as helping ordinary Americans save for retirement, including by proposing to automatically enroll workers in employer-sponsored retirement plans. But they also include perks for the retirement and financial industries, such as relaxing rules in ways that are seen as a boon for insurers. And buried deep inside the two complex bills are provisions that could make it harder for the IRS to crack down on the ultrawealthy who dodge tax rules.

by Justin Elliott, James Bandler and Patricia Callahan for ProPublica and published via Creative Commons License

The New Offering Will Take Off Fast, Based on the Perks and Details…

As with most things financial, there are lots of details, but some interesting perks, particularly for frequent customers of Apple products.

Immediate sign up on your iPhone

First perk: no lengthily complicated application process. According to the pre-launch information (see video above), just go to the Wallet app and tap on the Apple Card interface (once the Card is live) and go through the simple activation steps.

Once the sign up steps are complete, you can immediately start using the card as you would Apple Pay.

Small but expected caveat: For non-Apple Pay purchases in a traditional store setting you will need to wait until your physical card arrives in the mail. Also, although a pre-approved status will often be in place, availability is still subject to qualification, like any credit card.

Using the Card

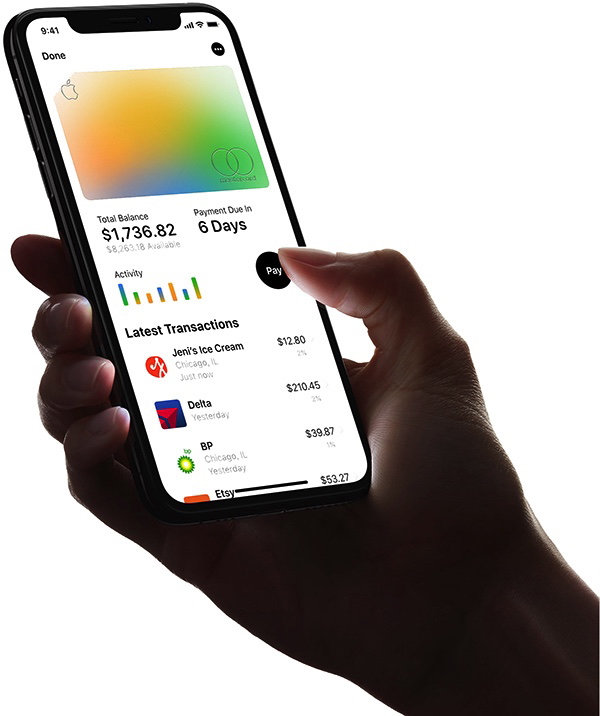

The card will function as would any other card in your wallet for Apple Pay. This includes online purchases and in-store checkout where you normally would use Apple Pay.

You can designate the Apple Card as your default payment method in your wallet for purchases using your iPhone, iPad, Mac or Apple Watch.

The extended uses for the digital and physical version of the card are enabled through the partnership between MasterCard and Apple. You will be able to use the Apple Card anywhere that a MasterCard is accepted.

Goldman Sachs is the credit provider for your Apple Card and they will set your interest rate based, as would be expected, on your current credit score. Rates are projected to be in the range of 13.24% to 24.24% which is below the average in the US.

An extended fixed payment system is likely to be offered for large purchases according to the pre-release data.

Main Perks and Advantages

There are many unconventional and improved aspects to the use and especially the user experience associated with the new card. In the keynote announcement earlier this year (see video above) a great emphasis was made on the ways that the project was focused on improving the experience and helping users attain a healthier financial lifestyle.

This includes various features designed to help reduce interest charges, not only by offering lower overall rates, but by giving the user options and calculations that can provide payment alternatives to the traditional “minimum monthly” payment currently the norm.

Payments can be made from your linked bank account or can be transferred from Apple Cash in your Wallet app.

There is no annual fee for the card, no international fees and no fee for exceeding your credit limit or making a late payment. Also, there is not increased interest rate penalty, per se, for late payment, which is common in some other credit card accounts. Late payment will, naturally, result in interest accrual, but based on your current rate.

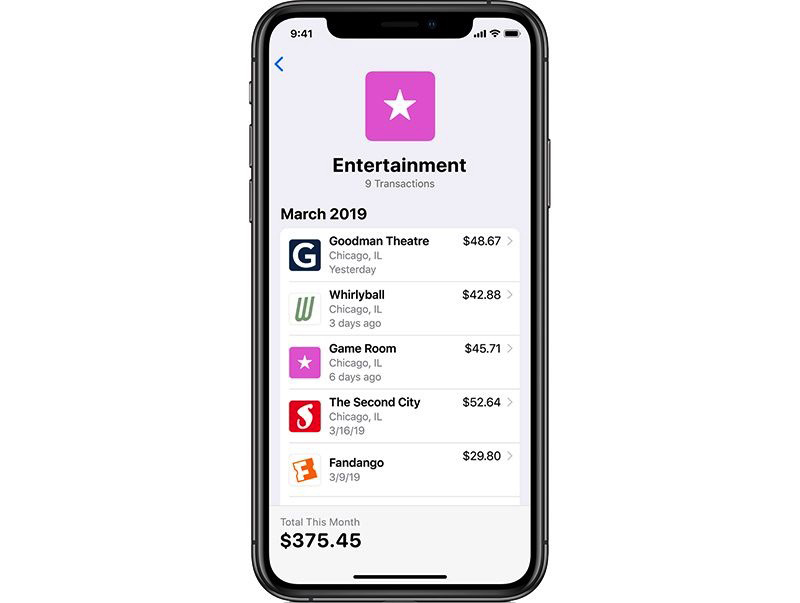

There is an separate app, particularly useful on iPad, which does not have the Wallet app, where data on transactions, payments and other details are provided. This, in typical Apple style, is far superior to any credit card app interface from banks and lenders.

Rewards and “Daily Cash”

Rather than a points system commonly seen on traditional credit card accounts, the Apple Card has a cash back system which can kick back up to 3% on a daily basis.

They call this “Daily Cash” and, as the name implies, your rebated cash will be credited to your account every 24 hours and be directly transferred to your Apple Cash account. If you do not sign up for Apple Cash, you will get your rebates sent to your bank account monthly.

Percentages vary, 3% is for all purchases made directly from Apple, 2% for all Apple Pay transactions and 1% for using the physical card at any non-Apple Pay retailer.

There is no cost to transfer your rewards cash to your bank account and this can take from one to three days. There will be an option to get instant transfers, which will incur a 1% fee. The transfers are done through the Apple Cash card from the Wallet app to the linked bank account.

Best Features and Conclusion

The overall sense is that this is going to be a very popular offering, based on the positive attributes of the card and the deal.

Although the terms are clearly slanted towards encouraging financial activity benefiting the emerging Apple financial eco-system, with the reward percentage on direct Apple purchases and Apple Pay coming in higher than the “out of network” transactions made with the physical card only, the rest of the perks are more than enough to pique the interest of a great number of iPhone users.

The titanium card appearance, styling and feel will attract many for that reason alone. Quel chic! And it is likely that the card will cause an increase in Apple Pay transactions, with double cash back for pulling out your iPhone instead of the physical card.

Ultimately, the software tools enabling privacy – no data to Apple and Goldman Sachs promising never to use or sell your data – along with the fantastic tools for tracking transactions, spend, payments and interest are perhaps the most likely to create love.

Who doesn’t hate dealing with credit card companies and their antiquated interfaces and systems? Some credit card providers do not even allow automatic payment scheduling, apparently hoping you will pay late so they can rack up those late payment penalty fees. Doing away with even the worst, most evil, aspects of credit card accounts is already a huge step forward.

Let’s hope that Apple will manage this as well as it appears. It looks like a top flight offering that has plenty of advantages that make it head and shoulders above the pack, and, for iPhone users it seems like a “must have” if there ever was one.

Easy sign-up on iPhone

Accepted worldwide (wherever Mastercard is available)

Up to 3% cash back

Daily cash back

No fees

Engraved Titanium physical card with concealed numbers