The pioneering spirit driving Elon Musk’s SpaceX to prepare for life on Mars is captivating, but a compelling alternative suggests we should use this same spirit to heal and nurture our home planet.

The sun, our local star, is central to this Earth-centric vision. According to NASA, Earth receives approximately 174 petawatts of incoming solar radiation in the upper atmosphere.

By efficiently harnessing just a fraction of this energy, we could significantly reduce our dependence on environmentally harmful fossil fuels.

Over the past decade, the cost of solar power has dramatically decreased and, with improvements in energy storage, (like Tesla’s Powerwall units, for example), solar energy is becoming a reliable, 24/7 power source.

Ephemeralization: Doing More with Less

However, the shift towards sustainable living extends beyond changing our energy source. This is where the principles of R. Buckminster Fuller, a visionary architect, systems theorist, author, designer, and inventor, come into play.

Fuller proposed the concept of “doing more with less,” forecasting a future where technological advancements lead to “ephemeralization,” a scenario in which we could fulfill everyone’s needs using fewer resources. This notion could help pave the way for a more environmentally sustainable world that also addresses issues of scarcity and inequality.

Building Efficiency: Embracing Integrative Design

Our journey towards a sustainable future is complemented by the principles of “integrative design,” a concept championed by Amory Lovins, co-founder of the Rocky Mountain Institute.

Lovins’ approach focuses on a holistic systems design where individual components work together in synergy, maximizing energy and resource efficiency.

This concept applies prominently to building efficiency, an area where Lovins has made significant contributions. By considering elements such as orientation, insulation, window placement, and ventilation, buildings can be designed to maintain comfortable temperatures with minimal active heating or cooling.

This “passive house” approach dramatically reduces energy consumption, making buildings part of the climate solution rather than a source of the problem.

Lovins’ approach also applies to manufacturing and industry, which, together, account for over 40% of total U.S. energy consumption.

By redesigning industrial processes to minimize waste, utilize waste heat, and prioritize energy-efficient equipment, Lovins argues that industries can dramatically reduce their energy use without sacrificing output or quality.

Taken to the furthest logical conclusion, the principles of integrative design could revolutionize how we conceive of energy use across all sectors.

Circular Economy and Soil Regeneration: Emulating Nature’s Cycle

To create a genuinely sustainable society, we need to redefine our economic systems and our relationship with the land. Our shift must be from a linear economic model—where we extract, use, and discard resources—to a circular one that mimics nature’s endless cycles of growth, decay, and renewal.

The Ellen MacArthur Foundation has been instrumental in leading efforts to establish an economy that is restorative and regenerative by design.

A key part of this shift involves regenerating our agricultural systems. Soil health is vital for maintaining biodiversity, water quality, and carbon sequestration.

Regenerative agriculture, including practices like cover cropping, no-till farming, and composting, can restore soil health and enhance its capacity to absorb carbon from the atmosphere.

According to the Rodale Institute, if current farmlands globally shifted to regenerative organic practices, it could sequester more than 100% of current annual CO2 emissions. Transitioning towards such practices could significantly mitigate climate change and rejuvenate our food systems.

Economic Justice: Power to All

An Earth-centric future also calls for economic justice. In a world powered by the sun, where resources are used wisely, waste is minimized, and the soil is restored, basic needs—such as healthcare, education, and equal opportunity—could be universally provided.

Establishing these rights is not just about altruism—it’s about creating a society where every individual can fully contribute to the collective good.

Mars Can Wait, But Can Earth?

The dream of a city on Mars is undoubtedly inspiring, but we must not overlook the opportunities beneath our feet. Our planet is not merely a stepping stone to the stars; it is a star in its own right.

Mars can wait, but can the Earth? With the elements for a sustainable revolution already within our grasp, it’s up to us to weave them together, creating a future that embraces both sustainability and economic justice.

The Long Road to an Earthly Future

The real odyssey, the true journey that demands our audacity and pioneering spirit, lies not in the red sands of a distant planet or under the shadows of unfamiliar stars. Instead, it unravels here, beneath the azure sky and upon the rich, verdant expanses of our home, Earth.

This journey may be long and fraught with challenges. The road toward a sustainable, just, and abundant future will require us to reassess our values, reinvent our systems, and redefine our relationship with the environment.

It calls for us to weave together principles of ephemeralization, integrative design, circular economy, soil regeneration, and economic justice into the fabric of our societies.

Yet, even as we embark on this formidable quest, we should remember that the destination is not merely a point in the future. It is a process, a continuous evolution that offers us countless opportunities for growth, learning, and reinvention.

Every step we take towards this envisioned future—whether it’s a solar panel installed, a passive house built, or a plot of land regenerated—brings us closer to realizing our potential as a species.

Unlike the cold, alien landscapes of Mars, the Earth provides us with a setting that is intimately familiar yet brimming with untapped potential.

We have the knowledge, the technology, and the means. All we need now is the collective will to channel our exploratory spirit inward, to heal, nurture, and transform the world we already have.

So let the red planet wait. For now, we have an extraordinary world under our feet, a world that we are yet to fully comprehend and appreciate.

Our gaze should not be fixed on distant celestial bodies, but on the potential lying dormant in our societies and within ourselves. The future of humanity is not just out there in the cosmos, but also right here, on the third rock from the Sun. The Earth and its promise of a sustainable and equitable future, is real, and attainable.

The Federal Reserve has begun its most challenging inflation-fighting campaign in four decades. And a lot is at stake for consumers, companies and the U.S. economy.

The challenge for the Fed is to do this without sending the economy into recession. Some economists and observers are already raising the specter of stagflation, which means high inflation coupled with a stagnating economy.

As an expert on financial markets, I believe there’s good news and bad when it comes to the Fed’s upcoming battle against inflation. Let’s start with the bad.

In all, Congress spent US$4.6 trillion trying to counter the economic effects of COVID-19 and the lockdowns. While that may have been necessary to support struggling businesses and people, it unleashed an unprecedented bump in the U.S. money supply.

At the same time, supply chains have been in disarray since early in the pandemic. Lockdowns and layoffs led to closures of factories, warehouses and shipping ports, and shortages of key components like microchips have made it harder to finish a wide range of goods, from cars to fridges. These factors have contributed to a worldwide shortage of goods and services.

Any economist will tell you that when demand exceeds supply, prices will rise too. And to make matters worse, businesses around the world have been struggling to hire more workers, which has further exacerbated supply chain problems. The labor shortage also worsens inflation because workers are able to demand higher wages, which is typically paid for with higher prices on the goods they make and the services they provide.

And now Russia’s war in Ukraine is compounding the problems. This is mostly because of the conflict’s impact on the supply of gas and oil, but also because of the sanctions placed on Russia’s economy and the ancillary effects that will ripple throughout the global economy.

The latest inflation data, released on March 10, 2022, is for the month of February and therefore doesn’t account for the impact of Russia’s invasion of Ukraine, which sent U.S. gas prices soaring. The prices of other commodities, such as wheat, also spiked. Russia and Ukraine produce a quarter of the world’s wheat supply.

Inflation won’t be slowing anytime soon

And so the Fed has little choice but to raise interest rates – one of its few tools available to curb inflation.

But now it’s in a very tough situation. After arguably coming late to the inflation-fighting party, the Fed is now tasked with a job that seems to get harder by the day. That’s because the main drivers of today’s inflation – the war in Ukraine, the global shortage of goods and workers – are outside of its control.

So even dramatic rate hikes over the coming months, perhaps increasing rates from about zero now to 1%, will be unlikely to make an appreciable impact on inflation. This will remain true at least until supply chains begin to return to normal, which is still a ways off.

Cars and condos

There are a few areas of the U.S. economy where the Fed could have more of an impact on inflation – eventually.

For example, demand for goods that are typically purchased with a loan, such as a house or car, is more closely tied to interest rates. The Fed’s policy of ultra-low interest rates is one key factor that has driven inflation in those sectors in recent months. As such, an increase in borrowing costs through higher interest rates should prompt a drop in demand, thus reducing inflation.

But changing consumer behavior can take time, and it’ll require more than a quarter-point increase in rates at the Fed. So consumers should expect prices to continue to climb at an above-normal pace for some time.

Higher interest rates also tend to reduce stock prices, as other investments like bonds may become more attractive to investors. This in turn may lead people invested in stock markets to reduce their spending because they feel less wealthy, which may help reduce overall demand and inflation. The effect is minimal, however, and would take time before you see the impact in prices.

That’s why I think it’s unlikely the U.S. will experience stagflation – as it did in the 1970s and early 1980s. A very aggressive increase in interest rates could possibly induce a recession, and lead to stagflation, but by sapping economic activity it could also bring down inflation. At the moment, a recession seems unlikely.

In my view, what the Fed is beginning to do now is less taking a big bite out of inflation and more about signaling its intent to begin the inflation battle for real. So don’t expect overall prices to come down for quite a while.

How do things really get done (or more often not) in Washington D.C.?

In a new video from Robert Reich, former secretary of labor and accomplished author, the sad subject of so-called ’gridlock’ in government is addressed. This perspective is particularly useful and helpful to consider since this year is an election year.

There’s an unfortunate lack of understanding regarding how things actually work and, more importantly what can be done about it.

Inequality Media, the Org, led by Robert Reich, that is responsible for this content, is putting out clear and incisive messages on topics like this on a weekly, sometimes daily basis. Getting these kinds of valuable messages out to places like YouTube, TikTok and social media is important at anytime. Now, in such a critical moment in our history, it’s essential.

Why doesn’t Congress get anything done?

Well, one chamber actually does. Hundreds of bills have been passed by the House of Representatives, but have been blocked from even getting a vote in the Senate. Bills like The Freedom to Vote Act, The John R. Lewis Voting Rights Advancement Act, The Equality Act, Background checks for gun sales, Reauthorizing the Violence Against Women Act, The Protecting the Right to Organize Act, The Build Back Better Act. The list goes on.

So why aren’t these crucial bills getting a vote in the Senate? Because the filibuster makes it impossible.

All told, the House passed over 200 bills in 2021 that have not been taken up in the Senate. Everything from investing in rural education to preventing discrimination against pregnant workers to protecting seniors from scams – bills that have real, tangible benefits for the public; bills that have widespread public support.

So don’t believe the media narrative that Congress is trapped in hopeless gridlock and both sides are to blame. One chamber of Congress, led by Democrats, is passing important legislation and delivering for the people. But Republicans in the Senate, and a handful of corporate Democrats, are hell-bent on grinding the gears of government to a halt.

Why are Senate Republicans doing this? Because their midterm strategy depends on it. Republicans are blocking crucial legislation so they can point to Democrats’ supposed inability to get anything done, and claim they’ll be able to deliver if you give them majorities.

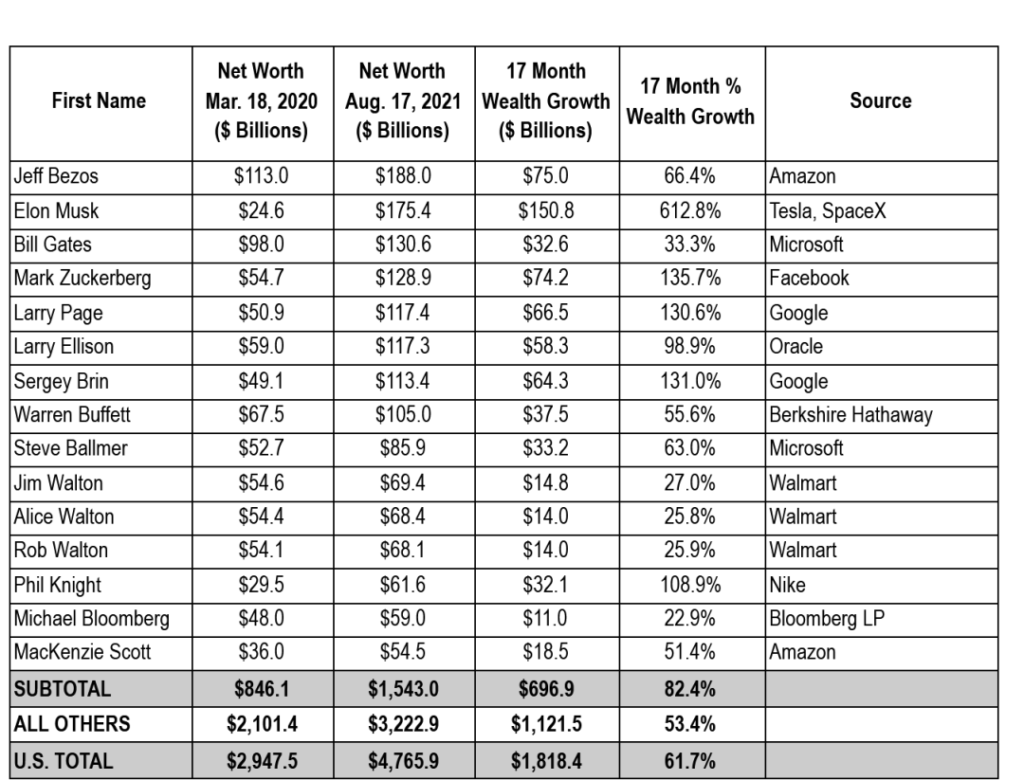

A new analysis finds that the 704 billionaires in the U.S. now own more wealth than the bottom half of Americans—roughly 165 million people.

During the first two years of the coronavirus pandemic, the collective wealth of billionaires in the United States grew by a staggering $1.7 trillion as Covid-19 killed millions of people across the globe and threw entire nations into turmoil, worsening extreme poverty, hunger, and other preexisting crises.

“We can’t accept an economy and tax code that allows billionaires to hoard trillions while working families struggle.”

Released Friday to coincide with the second anniversary of the World Health Organization’s official pandemic declaration for Covid-19, the latest billionaire fortune analysis by Americans for Tax Fairness (ATF) finds that the 704 billionaires in the U.S. now own more combined wealth than the 165 million people in the bottom half of the country’s wealth distribution.

“For billionaires, it’s been two years of raking in the riches, while for most families it’s been two years of fear, frustration, and financial worry,” ATF executive director Frank Clemente said in a statement.

The new analysis stresses that billionaires’ pandemic windfall “may never be taxed” because it consists of unrealized capital gains, which are not subject to taxation under current U.S. law. As one possible solution, ATF voices support for Sen. Ron Wyden’s (D-Ore.) proposed Billionaires Income Tax, legislation that would impose an annual levy on ultra-wealthy Americans’ unrealized gains from tradable assets such as stocks.

“The rising asset values billionaires have enjoyed over the past two years are not taxable unless the assets are sold,” ATF explains. “But billionaires don’t need to sell assets to benefit from their increased value: they can live off money borrowed at cheap rates secured against their rising fortunes. And when all those wealth gains are passed along to the next generation, they entirely disappear for tax purposes.”

This is why we need Congress to pass a Billionaires Income Tax.

It will tax billionaire wealth gains every year, just like workers’ wages are taxed. And it would raise $557 billion—more than enough to cover the historic clean energy investments @POTUS has proposed, for example.

— Americans For Tax Fairness (@4TaxFairness) March 11, 2022

While Democrats in Congress considered a tax on billionaires as part of their Build Back Better package, that legislation was tanked by a handful of corporate Democrats—including Sen. Joe Manchin (D-W.Va.)—and a unified Republican caucus.

“Why should our economic system allow billionaires to hoard wealth unchecked, letting almost all of it go tax-free?”

Earlier this month, Manchin floated a further watered-down version of the Build Back Better proposal that calls for tax reforms targeting the wealthy and corporations, but it’s unclear whether the West Virginia Democrat would accept a tax on billionaires.

“Working families pay what they owe in taxes each paycheck. Billionaires generally pay little or nothing in taxes on these extraordinary gains in wealth,” Clemente said Friday. “Congress should enact a Billionaires Income Tax to directly tax these wealth gains as income each year, so that billionaires begin to pay their fair share of taxes. Such a reform is not yet part of President Biden’s investment and tax legislation now being revised by Congress, but it should be.”

According to ATF’s new analysis, the biggest billionaire winners during the coronavirus pandemic’s first two years were:

Tesla and SpaceX CEO Elon Musk, who saw his net worth skyrocket by $209 billion;

Google co-founder Larry Page, whose fortune grew by $63 billion; and

Google co-founder Sergey Brin, whose wealth increased by $60 billion.

“Not one of the 15 richest U.S. billionaires gained less than $10 billion,” ATF noted on Twitter, pointing out that during the same two-year period 80 million Americans were infected by Covid-19 and nearly a million were killed by the virus.

“We can’t accept an economy and tax code that allows billionaires to hoard trillions while working families struggle to afford healthcare, childcare, education, and housing,” the group added. “It’s wrong, and we can do better.”

Originally published on Common Dreams by JAKE JOHNSON and republished under Creative Commons (CC BY-NC-ND 3.0

Bitcoin and Crypto’s reached a major turning point: why is cryptocurrency worth anything?

In a recent interview clip Jack Dorsey quietly states his opinion on the difference between people who “get” blockchain and crypto, and those that will forever be married to the past:

This is the simply stated portion that says it all:

“People who have questions in the world, people who have curiosity (and are) recognizing that the current systems, wether they be corporate financial systems or the government financial systems just aren’t working for them…”

Although the context of his statement is regarding bitcoin as the native currency for the internet, and in particular how people are responding to the fact that financial systems “just aren’t working for them” it is, nevertheless, a perfect statement of how the world is changing.

It has already changed into two distinct groups: those that are clinging to the status quo, since it has worked very well for them, and those that want to find a new and better way, because, in most cases, the current system did not work for them.

It’s important to realize that this statement is not coming from a disgruntled outsider, but from the hugely successful founder of Square, now called Block.

The fact that a large group of highly successful business leaders, such as Jack Dorsey and Elon Musk, although benefiting massively from the current financial systems, are at the same time embracing a new way of thought and action for the future, is at the crux of the issues addressed in this post.

Buffet vs Musk & Dorsey and the zero sum mindset of Malthusian Capitalism

There is a war waging between those that are open to, and welcoming of, bitcoin, crypto, blockchain, DeFi and other new financial innovations and those that reject all of it and would like nothing more than to see it stopped, by any means necessary.

The derision, insults and disdain lobbed at bitcoin, crypto and anyone that believes in them, by the “old guard” epitomized by Warren Buffet and Charlie Munger are now well known and documented:

A few quotes:

“Probably rat poison squared.” — Warren Buffett in Fox Business interview at 2018 meeting

“I think I should say modestly that the whole damn development is disgusting and contrary to the interests of civilization” – Charlie Munger vice chairman at Berkshire Hathaway

“I certainly didn’t invest in crypto. I’m proud of the fact I’ve avoided it. It’s like a venereal disease or something. I just regard it as beneath contempt.” – Charlie Munger vice chairman at Berkshire Hathaway

Interestingly, if you look deeper at the interviews and quotes, you’d see that, in spite of the headline grabbing hyperbole, it’s the price speculation that is at the heart of the criticism.

The comments that crypto and bitcoin “don’t produce anything” are ridiculous on their face, as if the fiat dollar “produces” products, services or anything else.

Oh, wait, the dollar does “produce” inflation (loss in value), and has done so very dependably over the last 100+ years.

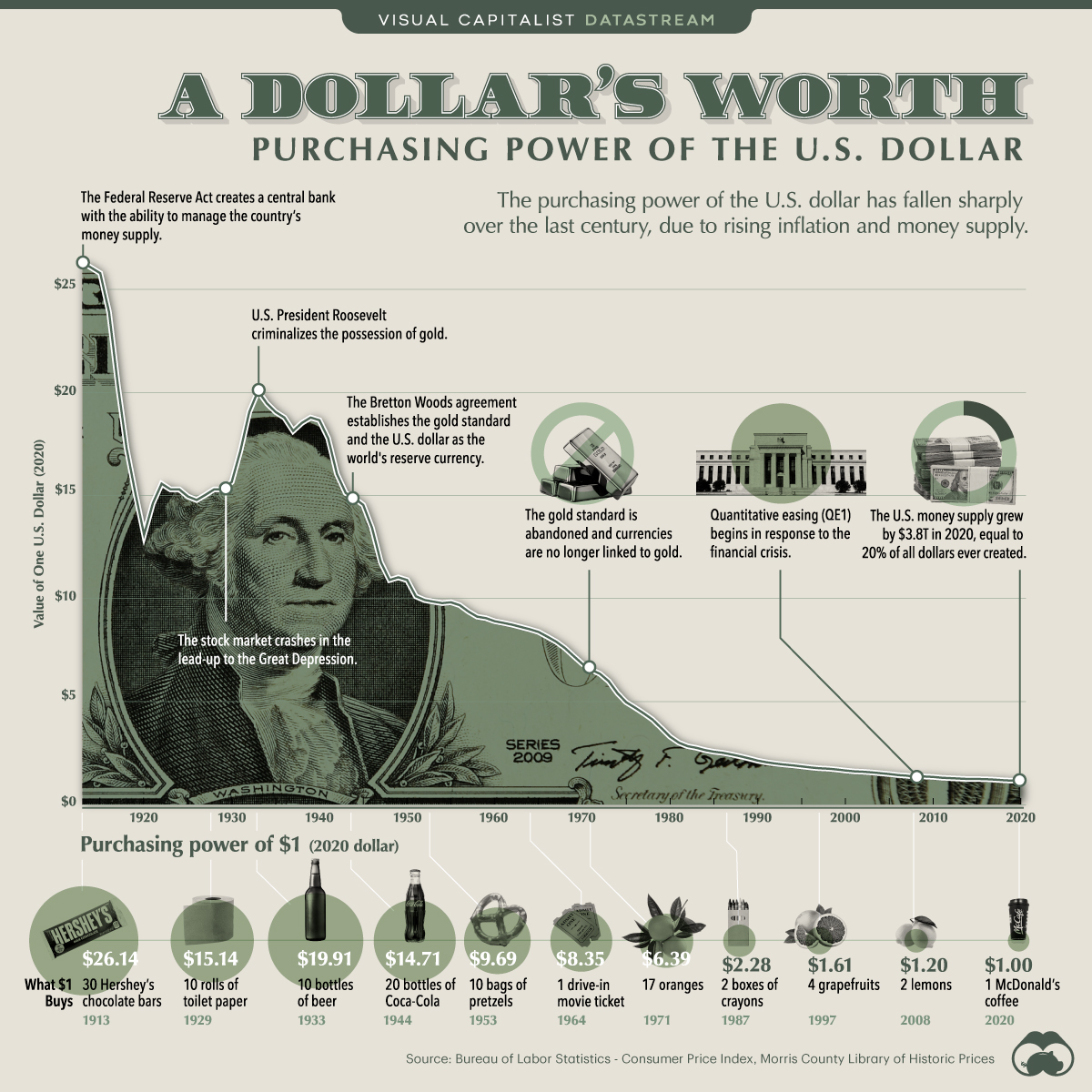

Take a stat so well known that it is almost a cliché, any way you put it: a 2013 U.S. dollar (the year the federal reserve was created, not coincidentally) would be worth more than 16x what a dollar is worth today. One has to ask where that value is now?

Bitcoin, however, has over time only gained value. A lot. If bitcoin is rat poison, maybe the fiat system and the federal reverse are the rat?

100 year old billionaires are, aparently, not inclined to speak from enlightened self-interest. Or, to be kind, perhaps they are blinded by the success they enjoyed in a system that favors anyone at the top of the pyramid, one built on value theft?

One very big caveat, however, is clearly that the “everything bubble” is bursting, price speculation always ends in price crashes, and the massive gains in the value of various cryptocurrencies are a symptom of a larger systemic emergency, rather than a quality inherent to crypto itself. There’s that.

The gap between this kind of thinking vs. that of the forward looking cryptocurrency proponents, and what they consider to be positive innovations, is vast. In a time where divisive thought is nearly ubiquitous this is not news.

However, the fact that the legions of those that “get it” are as large as they are, and that they are constantly growing, has clearly taken the debate past the point of no return.

To get the full view of this divide it’s important to look also at just how the nearly 100 year old duo of Buffet & Munger got to be the “legends” that they are.

All the best known names they are associated with, from the initial Berkshire Hathaway purchase in 1962 to more recent investments in companies such as CocaCola, GEICO Insurance, RJ Reynolds Tobacco, Sees Candy, Clayton Homes and so on, paint a clear picture of extreme hierarchal and exploitative capitalism that is solely based on making themselves and shareholders rich, and doing it on the backs of consumers.

In an example of the thinking of those that do not worship the duo, in The Nation, David Dayen wrote: “America isn’t supposed to allow moats, much less reward them. Our economic system, we claim, is founded on free and fair competition. We have laws over a century old designed to break up concentrated industries, encouraging innovation and risk-taking. In other words, Buffett’s investment strategy should not legally be available, to him or anyone else.”

Exactly this kind of double standard, corrupt to the core, is built on systemic greed founded on a Malthusian “zero-sum mindset”. This is what has led millions to conclude that the system just isn’t working for them.

Being championed ad nausea for this lifetime of “achievement” is part and parcel of the status quo that many, from many in the 99% to the “nouveau 1%”, such as Elon Musk, Jack Dorsey, Vitalik Buterin and many others, are actively seeking alternatives to.

That distinction, being rich and powerful and yet not satisfied with the legacy of corruption and greed, is at the heart of the new wave of thought that has made bitcoin, crypto and DeFi a force to be reckoned with.

Moreover, seeing the state of the world that centuries of this kind of thinking has engendered, it’s natural for the young and more enlightened to want to search for other ways for things to work, ways that perhaps champion something other than monopolistic greed and exploitation.

In a recent Interview Elon Musk addressed precisely this issue – how many in the current system are focused on prospering at the expense of others and maintaining a zero-sum mindset. In the clip he outlines how important it is to understand the failure of that approach.

The idea that crypto will disappear is wishful thinking by those that cling to the systems of the past

A clip of Harrison Ford speaking at the Global Climate Action Summit was banned on some platforms as incendiary. Why? Because he passionately accuses those that are financially linked to fossil fuels of working to spread disinformation and misinformation, in order to perpetuate their massive incomes, even while the planet is on the brink of climate disaster.

Blocking this opinion, from a rich and famous film star, no less, is typical in the way that the established system works to suppress the idea that you should do anything about the fact that “it’s just not working” for you.

This is the same divide, mentioned above, that is nearly all pervasive today, but will never stop innovation in thinking about financial systems. It will not stop DeFi or DAOs or crypto or bitcoin.

It will not stop sustainable energy from becoming an ever bigger part of the world’s energy infrastructure. The point of going back has long since passed.

How money works according to Musk

Jack Dorsey has an understated and somehow “quiet” way of expressing revolutionary ideas. Elon Musk, on the other hand, is well known for controversial and flamboyant statements, and especially tweets.

But to get a taste of just how radical his thinking really is, particularly to those that disagree, you have to dig deeper into lengthy interviews, such as those with Lex Fridman, where he reveals his thinking more specifically on money, crypto and the governments role in the system of money.

Coming from the wealthiest person on earth, some may find it odd, yet his thoughts on crypto vs fiat money are well documented. It’s just this kind of stance, taken by so many in the “new” establishment at the top of the current financial pyramid, who also see the necessity for change toward new ideas and systems that can so away with the worst of the status quo, well represented above by Buffet & Munger and other “crypto haters”.

Government is a corporation in the limit

In yet another interview excerpt, Musk goes even deeper into his belief that – in his exact words: “if you don’t like corporations should really hate governments”

While this particular statement arose out of a spat with Senator Elizabeth Warren regarding taxes, the overall concept of challenging the status quo and the, clearly failed, systems perpetuated, remains in play.

Web3, and how Web2 and legacy financial structures are linked

Although fraught with infighting – the typical bitcoin vs. Ethereum vs. Doge vs. Shiba Inu internal debates and criticisms are not on the magnitude of the division between those that generally support and benefit from, for example, status quo financial structure and fossil fuel business, vs those that favor Blockchain and Sustainable energy.

Further, the spirit of the clash between Web2 and Web3 rests not on the tech or the systems themselves, which it can be argued are the same, but on the beliefs and intent of each camp.

The surveillance capitalism business models of web2, epitomized by Facebook and Google are diametrically opposed to the spirit and stated goals of web3, just as bitcoin was created out of a time that, not coincidentally, corresponded to the 2008 crash and crisis born of the greed and corruption of the legacy economic establishment.

There are two distinct camps that have emerged.

Those, such as Tesla and Elon Musk, that reject the traditional holy grail of shareholder value and instead embrace, for example, a more enlightened mission “to accelerate the transition to sustainable energy”. This aligns with any individual choosing the support crypto as a “Hodler” or at least believer, vs. those that support the legacy systems of finance, the fossil fuel industrial complex and Web2’s exploitative business model.

This divide is the ultimate test of our time and it will only grow in stature and importance.

The correspondence between forward looking innovation in all human thought, communication and action is already too big to stop and cannot be wished away.

There will undoubtedly be setbacks to these new directions, and there will be attacks using more than insults, such as those quoted above, but the time for the unstoppable force to be quelled is long since past. Coke and a smile? No thanks.

In a new video from Robert Reich, former secretary of labor and accomplished author, the phenomena we are all experiencing on a daily basis, such as incredible high gas prices, crazy energy prices, more out-of-pocket at the grocery store, and what sure looks like price gouging and price hikes on almost everything, he takes on the root of it all, in other words: Inflation.

Naturally, with all of this being so obvious to you and me there’s no shortage of folks to explain the purported causes, from media outlets like The Washington Post, to Biden administration officials and pundits from left, right and center.

One explanation you will seldom hear, however, is that much of the pain we are experiencing is due to monopoly power, the inequality growing out of the economic concentration of the American economy and the ever increasing concentration of financial and market power to a relative handful of big corporations.

This perspective is not only refreshingly direct, but it actually has a remedy attached, unlike the usual reasons given, such as economic policy, government spending, irresponsible actions by the federal government and federal reserve and so on. While all of these are certainly good candidates for finger pointing, they generally have only one response attached that is suggested as a remedy: higher interest rates.

“How can this structural problem be fixed? Fighting corporate concentration with more aggressive antitrust enforcement. Biden has asked the Federal Trade Commission to investigate oil companies, and he’s appointed experienced antitrust lawyers to both the FTC and the Justice Department.”

– Robert Reich

The idea that corporate greed, massive corporate profits that keep rising, in spite of supply chain disruptions and other issues, could be at the root of the problems, and that aggressive use of antitrust law might just be an appropriate response to the deeper structural issue is spot on.

A real change via antitrust might help to reinstate tough competition, weed out greedy businesses and even slow down the increasing consolidation of the economy, and the concept comes across as a welcome revelation, or at least beats a job and economy crushing series of Paul Volcker-style (huge) interest rate hikes.

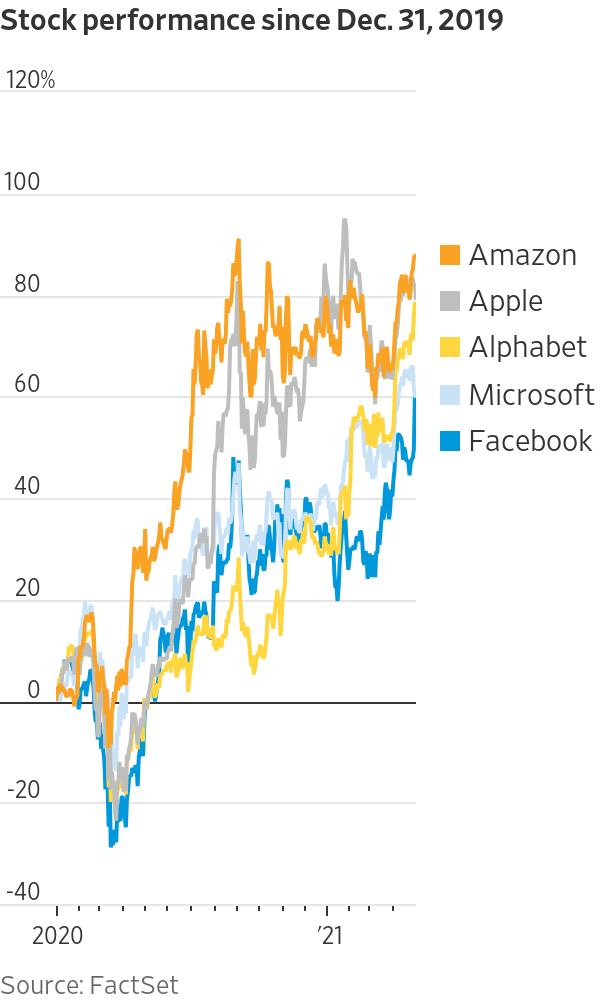

There’s an even bigger challenge on the horizon, however, which is the sheer size of the biggest tech firms, who make the companies mentioned in the video, such as Coke, Pepsi, Procter & Gamble, meat conglomerates and the pharmaceutical industry seem tiny by comparison. As noted by the Wall Street Journal, during the pandemic the behemoths such as Facebook, Amazon and Microsoft have surged.

This is evidence of even less competition than in the sectors mention and presented in the video, and yes, the energy sector, consumer goods, food prices are all showing little competition and that situation is getting worse.

At least we have Mark Zuckerberg, from a recent YouTube interview with Lex Fridman, with his sunny personality shining through, saying that “what if playing with your friends is the point [of life]?, and further “I think over time, as we get more technology, the physical world is becoming less of a percent of the real world, and I think that opens up a lot of opportunities for people because you can you can work in different places you can stay closer to people who are in different places removing barriers of geography”. At least, then, there’s that. Thanks Mark.

The video text reads well also on the page. Charts, graphics and the charismatic voice of Robert Reich are worth the watch, but here is the full text, in case you prefer:

Inflation! Inflation! Everyone’s talking about it, but ignoring one of its biggest causes: corporate concentration.

Now, prices are undeniably rising. In response, the Fed is about to slow the economy — even though we’re still at least 4 million jobs short of where we were before the pandemic, and millions of American workers won’t get the raises they deserve. Republicans haven’t wasted any time hammering Biden and Democratic lawmakers about inflation. Don’t fall for their fear mongering.

Everybody’s ignoring the deeper structural reason for price increases: the concentration of the American economy into the hands of a few corporate giants with the power to raise prices.

If the market were actually competitive, corporations would keep their prices as low as possible as they competed for customers. Even if some of their costs increased, they would do everything they could to avoid passing them on to consumers in the form of higher prices, for fear of losing business to competitors.

But that’s the opposite of what we’re seeing. Corporations are raising prices even as they rake in record profits. Corporate profit margins hit record highs last year. You see, these corporations have so much market power they can raise prices with impunity.

So the underlying problem isn’t inflation per se. It’s a lack of competition. Corporations are using the excuse of inflation to raise prices and make fatter profits.

Take the energy sector. Only a few entities have access to the land and pipelines that control the oil and gas powering most of the world. They took a hit during the pandemic as most people stayed home. But they are more than making up for it now, limiting supply and ratcheting up prices.

Or look at consumer goods. In April 2021, Procter & Gamble raised prices on staples like diapers and toilet paper, citing increased costs in raw materials and transportation. But P&G has been making huge profits. After some of its price increases went into effect, it reported an almost 25% profit margin. Looking to buy your diapers elsewhere? Good luck. The market is dominated by P&G and Kimberly-Clark, which—NOT entirely coincidentally—raised its prices at the same time.

Another example: in April 2021, PepsiCo raised prices, blaming higher costs for ingredients, freight, and labor. It then recorded $3 billion in operating profits through September. How did it get away with this without losing customers? Pepsi has only one major competitor, Coca-Cola, which promptly raised its own prices. Coca-Cola recorded $10 billion in revenues in the third quarter of 2021, up 16% from the previous year.

Food prices are soaring, but half of that is from meat, which costs 15% more than last year. There are only four major meat processing companies in America, which are all raising their prices and enjoying record profits. Get the picture?

The underlying problem is not inflation. It’s corporate power. Since the 1980s, when the U.S. government all but abandoned antitrust enforcement, two-thirds of all American industries have become more concentrated. Most are now dominated by a handful of corporations that coordinate prices and production. This is true of: banks, broadband, pharmaceutical companies, airlines, meatpackers, and yes, soda.

Corporations in all these industries could easily absorb higher costs — including long overdue wage increases — without passing them on to consumers in the form of higher prices. But they aren’t. Instead, they’re using their massive profits to line the pockets of major investors and executives — while both consumers and workers get shafted.

How can this structural problem be fixed? Fighting corporate concentration with more aggressive antitrust enforcement. Biden has asked the Federal Trade Commission to investigate oil companies, and he’s appointed experienced antitrust lawyers to both the FTC and the Justice Department.

So don’t fall for Republicans’ fear mongering about inflation. The real culprit here is corporate power.

Early in 2020, as the pandemic gripped the nation, JPMorgan Chase offered to help customers weather the crisis by taking a temporary pause on mortgage, auto and credit card payments. Chase’s CEO, Jamie Dimon, sounded sympathetic about a year later as he offered broader reflections on what was ailing the country. “Americans know that something has gone terribly wrong,” he wrote in a letter to shareholders. “Many of our citizens are unsettled, and the fault line for all this discord is a fraying American dream — the enormous wealth of our country is accruing to the very few. In other words, the fault line is inequality.”

But even as those words were published, the bank had quietly begun to unleash a lawsuit blitz against many of its struggling customers. Starting in early 2020 and continuing to today, Chase has filed thousands of lawsuits against credit card customers who have fallen behind on their payments.

Chase had stopped pursuing credit card lawsuits in 2011, in the wake of the last major economic downturn, after regulators found that the company was filing tens of thousands of flimsy suits, sometimes overstating what customers owed. Rather than being backed by extensive billing records to document the debts, according to the regulators, the suits were typically filed with a short affidavit from one of a half-dozen Chase employees in one office in San Antonio who vouched for the accuracy of the bank’s information in thousands of suits.

Chase “filed lawsuits and obtained judgments against consumers using deceptive affidavits and other documents that were prepared without following required procedures,” the Consumer Financial Protection Bureau concluded in 2015. At times, Chase employees signed affidavits “without personal knowledge of the signer, a practice commonly referred to as ‘robo-signing.’” According to the CFPB’s findings, there were mistakes in about 10% of cases Chase won and the judgments “contained erroneous amounts that were greater than what the consumers legally owed.”

Chase neither admitted nor denied the CFPB’s findings, but it agreed, as part of a consent order, to provide significant evidence to make its cases in the future. The company also agreed it would provide “relevant information and documentation maintained by [Chase] to support their claims” in cases — the vast majority of those it filed — in which customers did not respond to the lawsuit.

But that provision expired on New Year’s Day 2020. And since then the bank has gone back to bringing lawsuits much as it did before 2011, according to lawyers who have defended Chase customers.

“From what I can see, nothing has changed,” said Cliff Dorsen, a consumer-rights attorney in Georgia who represents Chase credit card customers.

Chase declined to make executives available for interviews. It said in a statement that the timing of the resumption of its credit card lawsuits was just a coincidence. “We have engaged with our regulators throughout this process,” said Tom Kelly, a bank spokesperson. “We continue to meet the requirements of the consent order.” (Kelly said Chase also filed some credit card lawsuits in 2019.)

Kelly declined to say how many suits it has filed in its blitz of the past two years, but civil dockets from across the country give a hint of the scale — and its accelerating pace. Chase sued more than 800 credit card customers around Fort Lauderdale, Florida, last year after suing 70 in 2020 and none in 2019, according to a review of court records. In Westchester County, in New York’s suburbs, court records show that Chase has sued more than 400 customers over credit card debt since 2020; a year earlier, the equivalent figure was one.

A similar surge is occurring in Texas, according to January Advisors, a data-science firm. Chase filed more than 1,000 consumer debt lawsuits around Houston last year after filing only seven in 2020, the analytics firm’s review of court records in Harris County shows. Chase instigated 141 consumer debt cases in Austin last year after filing only one such case in 2020, according to January Advisors, which is conducting research for a nationwide study ofdebt collection cases.

Today, just as it did before running afoul of the CFPB, Chase is mass-producing affidavits from the same San Antonio office where low-level employees generated hundreds of thousands of affidavits in the past, according to defense attorneys and court documents. Those affidavits are often the main piece of evidence that Chase uses to win its case while detailed customer records — and any errors they may contain — remain out of sight.

“Our clients deserve to see everything that Chase has in its files,” Dorsen said. “Instead, Chase gives us these affidavits and says: ‘You can trust us about the rest.’”

Before the robo-signing scandal a decade ago, Chase recovered about a billion dollars a year with its credit card collections business, according to the CFPB. Why would Chase stop suing customers for years, forgoing billions of dollars, only to ramp up its suits once key provisions of the CFPB settlement had expired?

Craig Cowie thinks he has an answer. “Chase did not think it could make money if it had to sue customers and abide by the CFPB settlement,” said Cowie, who worked as an enforcement attorney at the CFPB during the Obama administration and now teaches at the University of Montana Law School. “That’s the only explanation that makes sense for why the bank would have held back.”

Cowie, who did not work on the CFPB’s case against Chase, said he doesn’t know why the agency agreed to a time limit on some settlement provisions. He pointed out that such agreements are negotiated and the CFPB cannot just dictate the terms. The agency may have felt it had to let some provisions of the settlement expire to get Chase to agree to the deal, Cowie said.

The CFPB declined to comment.

For its part, Chase said it waited years to restart its lawsuits because it took that long to get the system working right. “We rebuilt the litigation program slowly and methodically to make sure we had the right controls in place,” said its spokesperson, Kelly.

At the time, the CFPB had found numerous flaws in Chase’s suits. The agency concluded that Chase used “unfair” legal tactics when it promised that its credit card account information was reliable and mistake-free. It wasn’t simply a matter of errors in calculating how much was owed; in some cases the company even got the customer’s name wrong. Chase would sometimes pass accounts with errors — including instances where customers had been victims of credit card fraud, others who had tried to settle their debts and even some who had died — on to outside debt collectors, who might then take action based on that information.

Once Chase won a victory in court, the bank could seek to garnish a customer’s wages or raid their bank accounts, and those customers would pay a further price: a stain on their credit report that could make it harder to “obtain credit, employment, housing, and insurance,” the CFPB wrote.

Those sued by Chase, then and now, might spot errors if the company provided full records in its court filings, consumer advocates say. Instead, Chase typically submits copies of a few credit card statements along with a two-page affidavit attesting that the bank’s records were accurate and complete.

Consumer advocates say they do not expect that the majority of Chase’s credit card records are tainted with errors. But if today’s error rate is the same 10% that the CFPB estimated in the past and the Chase lawsuit push continues, thousands of customers may be sued for money they don’t owe. And there is no easy way to check when Chase keeps so many of its records out of sight.

Chase said that its current system for processing credit card lawsuits is sound and reliable. “We quality-check 100% of our affidavits today,” the company said in a statement.

Credit card customers do not respond to collections lawsuits in roughly 70% of cases, according to research from The Pew Charitable Trusts. In those instances, the customer typically loses by default.

In the small percentage of cases where a customer gets a lawyer or otherwise fights back, Chase still has the advantage because it can access all of the customer’s account records easily, according to consumer lawyers. (The bank typically closes accounts of customers who have failed to pay their debts, leaving them unable to access their records online.) Chase usually shares the complete credit card account file only after a legal fight, according to attorneys and pleadings from across the country. “Chase has all the evidence and we have to beg to get it,” said Jerry Jarzombek, a consumer-rights attorney in Fort Worth, Texas, who is defending several Chase customers.

The result leaves many defendants in a bind: They don’t have enough information to know whether they should dispute the company’s claims. “Chase wants us to believe its records are reliable so we don’t need to see them,” Jarzombek said. “Well, I’m sorry. I’ve dealt with Chase for decades. I’d prefer to see what evidence they’ve actually got.”

The robo-signing scandal exposed Chase’s affidavit-signing assembly line. Before the settlement, Chase had about a half-dozen employees churning through affidavits stacked a foot high or taller, according to the former Chase executive who brought the practices to light at the time. Kamala Harris, who was then California’s attorney general and is now vice president, likened the process to anaffidavit mill.

The current operation involves roughly a dozen “signing officers” working from the same San Antonio offices as before and performing many of the same tasks, according to Chase employees and outside lawyers who have represented the company.

Chase used to prepare affidavits “in bulk using stock templates,” according to the 2015 CFPB findings. That is again happening today, according to two of Chase’s outside lawyers who requested anonymity because they were not authorized to discuss the process.

The lawyers said they typically send their affidavit requests in batches. The requests already contain the basic details of the customer’s account when they arrive in Chase’s San Antonio office, they said. An affidavit request that is sent one day can typically be processed and returned the next business day, the lawyers said.

Chase affidavits contain stock language that the “signing officer” has “personal knowledge of and access to [Chase’s] books and records.” That “personal knowledge” is limited, said one signing officer who declined to be named. Chase does not expect signing officers to perform a forensic review of an account but rather to follow computer prompts to complete the affidavit, said the employee. “We just work with what’s on the screen.”

Chase declined to discuss its process for creating affidavits, but the bank said it satisfies the rules set by courts in the places where it operates. “Judges, clerks and other judiciary staff are well versed in the court rules and laws in their jurisdictions,” said the statement by the bank’s spokesperson, Kelly. “Through our counsel, we provide the information those parties require in matters before them.”

Courts around the country have grown too accepting of what big banks and debt collectors say, according to consumer advocates. And the justice they dispense can feel as cursory and hurried as the suits that Chase files.

In Texas a decade ago, lawmakers pushed most credit card cases into the state’s version of small claims courts, known as justice courts. The rules of evidence are more lax there and the judge might not even be a lawyer. A retired basketball player presides over one suchcourtroom in Houston. “One of these judges said to me: ‘What’s the point of seeing a bunch of evidence? We already know these people borrowed the money,’” said Jarzombek, the Fort Worth attorney. “I said: ‘Why even have a trial, then? Let the banks take whatever they want.’”

In Houston, where Chase has more than 1,000 consumer credit suits on the docket, only one defendant in those cases has fought to a trial on her own, according to court records.

That person’s experience is instructive. Like many, Melissa Razo struggled financially during the early pandemic. A former restaurant manager, the 42-year-old Razo had gone back to school, the University of Houston, to study psychology, and she supported herself by doing typing for an online transcription service. That work suddenly dried up when the pandemic hit, and Razo began missing credit card payments. Her debt escalated. Chase sued her in January 2021, claiming she owed a total of about $8,500 on two credit cards.

Razo had a previous court experience stemming from an acrimonious divorce, where she had learned that a plaintiff needs facts and evidence to win. “Nothing I presented was good enough,” she recalled of the divorce case.

Using what she’d learned, Razo prepared for her day in court against Chase. She could not access her account anymore, she said, because the bank had shut it down. So in late June, as her hearing date approached, Razo pulled together as many of her credit card statements as she could find. They told a story of grocery runs and shopping at Target and Goodwill, along with missed payments and penalties.

Razo presumed Chase would have to back up its claims just as she had been expected to do in divorce court. She expected the company’s lawyers would have five years of statements and documents to show that she owed exactly what they said she owed. This was a trial, after all.

The trial lasted perhaps a minute, according to Razo. It boiled down to two questions. Was Razo present? the judge asked over Zoom. When she announced herself, the judge asked if she had a Chase credit card. Yes, Razo said, that was true. Then, she said, the judge ruled in favor of Chase.

Chase declined to comment on the case. The judge was not authorized to speak about the matter, according to a court clerk. And the justice courts do not transcribe their hearings, so ProPublica could not verify what was said. (The court’s docket did confirm that a judgment was entered in Chase’s favor after a judge trial.)

Razo’s courtroom experience, though, sounds typical, according to Rich Tomlinson, a lawyer with Lone Star Legal Aid. “I can’t recall ever seeing a live witness in a debt case,” said Tomlinson, who has represented hundreds of debtors in his career. “These trials are not like Perry Mason. They’re not even Judge Judy.”

ProPublica is a Pulitzer Prize-winning investigative newsroom. Sign up for The Big Story newsletter to receive stories like this one in your inbox.

As a member of Congress, Jared Polis was one of the loudest Democrats demanding President Donald Trump release his tax returns.

At a rally in Denver in 2017, he warned the crowd that Trump “might have something to hide.” That same year, on the floor of the House, he introduced a resolution to force the president to release the records, calling them an “important baseline disclosure.”

But during Polis’ successful run for governor of Colorado in 2018, his calls for transparency faded. The dot-com tycoon turned investor broke with recent precedent and refused to disclose his returns, blaming his Republican opponent, who wasn’t disclosing his.

Polis may have had other reasons for denying requests to release the records.

Despite a net worth estimated to be in the hundreds of millions, Polis paid nothing in federal income taxes in 2013, 2014 and 2015. From 2010 to 2018, his overall rate was just 8.2% — less than half of the 19% paid by a worker making $45,000 in 2018.

The revelations about Polis are contained in a trove of tax information obtained by ProPublica covering thousands of the nation’s wealthiest people. The Colorado governor is one of several ultrarich politicians who, the data shows, have paid little or no federal income taxes in multiple years, exploited loopholes to dodge estate taxes or used their public offices to fight reforms that would increase their tax bills.

The records show that rich Democrats and Republicans alike have slashed their taxes using strategies unavailable to most of their constituents. Among them are governors, members of Congress and a cabinet secretary.

Richard Painter, the chief White House ethics lawyer during the George W. Bush administration, said the tax avoidance of these top politicians is “very, very worrisome” since both parties “spend like crazy” and depend on taxes to fund their priorities, from the military to Medicare to Social Security.

“They have the power to decide how much the rest of us pay and the power to spend the money, and then they’re not paying their fair share?” Painter said. “That should be troubling to voters, both conservative and liberal. It should be troubling for everyone.”

West Virginia Gov. Jim Justice, for example, is a Republican coal magnate who has made the Forbes list of wealthiest Americans. Yet he’s paid very little or no federal income taxes for almost every year since 2000.

California Rep. Darrell Issa, one of the richest people in Congress, was one of the few Republicans to break with his party during the 2017 tax overhaul to fight for a deduction that — unbeknownst to the public — helped him avoid millions in taxes.

And the tax records of Republican Sen. Rick Scott of Florida and Trump’s education secretary, Betsy DeVos, showed that both employed a loophole, which was accidentally created by Congress, to escape estate and gift taxes.

As ProPublica has revealed in a series of articles this year, these tactics, if sometimes aggressive, are completely legal. And they’re not universal among wealthy politicians. ProPublica reviewed tax data for a couple dozen wealthy current and former government officials. Their data shows that many of them paid relatively high tax rates while employing more modest use of the fairly standard deductions of the rich.

The politicians who paid little or exploited loopholes either defended their practices as completely proper or declined to comment.

“The Governor has paid every cent of taxes he owes, he has championed tax reform and tax fairness to fix this broken system for everybody, to report otherwise would be inaccurate,” Polis’ spokesperson wrote in an email.

During the late 1990s dot-com era, Polis earned a reputation as a boy wonder. He turned his parents’ small greeting card company into a website, bluemountain.com, which was among the first to enable users to send free virtual cards. He and his family sold the site in 1999 for $780 million.

With the windfall from the sale, Polis continued to start new ventures and invest, but he also began laying the groundwork for a career in politics. He landed in the governor’s office in 2019 when he was just 43.

One of his tools for raising his profile was philanthropy. His generous donations to charity became a theme of both his 2008 run for Congress and his 2018 run for Colorado’s highest office.

Philanthropy also helped keep his tax rate enviably low. In many years, the deductions he claimed for his charitable giving were large enough to wipe out half the income he would have owed taxes on. His giving allowed him, in essence, to take some of the money he would have paid into the public coffers and donate it instead to causes of his choosing.

But an examination of Polis’ philanthropy shows that while he has given to a wide variety of causes, some of his donations served to promote him, blurring the lines between charity and campaigning.

According to the tax filings of his charity, the Jared Polis Foundation, the organization spent more than $2 million from 2001 to 2008 on a semiannual mailer sent to “hundreds of thousands of households throughout Colorado” that was intended to build “on a foundation of familiarity with Jared Polis’ name and his support of public education.” It was one of the charity’s largest expenditures.

A 2005 edition of the mailer reviewed by ProPublica had the feel of a campaign ad. It was emblazoned with the title “Jared Polis Education Report,” included his name six times on the cover and featured photos of Polis, a former state board of education member, surrounded by smiling school children.

The newsletters were discontinued just as he was elected. Because the mailers did not explicitly advocate for his election, they would have been legally allowed as a charitable expenditure.

A decade later, when he ran for governor in a race that he personally poured more than $20 million into, Polis featured his philanthropy in his campaign. In one ad, he used testimonials from an employee and a graduate of a business training charity he founded for military veterans.

Polis’ spokesperson, Victoria Graham, defended the mailers, saying they were intended “to promote innovations and successful models in public education and to raise awareness for the challenges facing public education.” She also pointed to a range of other philanthropy Polis was involved in, from founding charter schools, which she noted were not named after him, to distributing computers to organizations in need.

“His philanthropy is not and has never been motivated by receiving a tax write-off, and to state otherwise is not only inaccurate but fabricating motives and intent and cynical in its view of charity,” Graham said.

While Polis’ charitable giving has helped keep the percentage of his income he pays in taxes low, he has also been able to keep his total taxable income relatively small by using another strategy common among the wealthy: investing in businesses that grow in value but produce minimal income.

It sounds counterintuitive, but it’s a basic principle of the U.S. tax system — one that typically benefits wealthy people who can afford not to take income. Investments only trigger income taxes when they produce “realized” gains, such as dividends from a stock holding, the sale of an asset or profits from a company. But an investment’s growth in value, while it makes its owner richer, is not taxable.

Polis acknowledged his use of the strategy in 2008 after he released tax information during his first run for Congress and faced criticism for paying so little in taxes. “I founded several high-growth companies, and we would manage those for growth rather than for profit,” he said. “When I make money, I pay taxes. When I don’t make money, I don’t.”

In one of the recent years Polis paid no income taxes, his losses were larger than his income. In two of the years, it was about a million dollars. From 2010 to 2018, when he paid an overall rate of just 8.2%, including payroll taxes, his income averaged $1.5 million.

During that period of low taxes and relatively low income, Polis’ estimated net worth rose sharply. Members of Congress only have to report the value of each of their assets in ranges, so assigning a precise number is impossible. But the nonprofit data site OpenSecrets, which makes estimates by taking the midpoint of the ranges, shows Polis’ wealth growing from $143 million in 2010 to $306 million in 2017, making him the third richest-member of the House at the time. (Graham said congressional disclosure forms are confusingly formatted, potentially causing certain assets to be counted more than once, “so these numbers are likely wildly off.” She did not provide alternative net worth figures.)

One of Polis’ primary vehicles for building his fortune, while avoiding taxable income, appears to have been a family office, Jovian Holdings. The board of directors included his father, sister and a rather surprising outsider: Arthur Laffer. The famed conservative economist’s Laffer Curve provided the Reagan administration with the intellectual basis for arguing that cutting taxes would increase tax revenue. (Polis’ sister is a ProPublica donor.)

The term family office has a mom-and-pop feel, but it is actually part of the infrastructure of protecting the fortunes of the ultrawealthy, from crafting investment and tax strategy to succession and estate planning to concierge services. Depending on how they’re organized, for instance as a business, their costs — the salaries of the staff, rent — can be deductible.

One of the executives at Polis’ family office, according to her LinkedIn profile, is a seasoned tax expert who specializes in “maximizing cost savings both operationally and with all taxing authorities.” She removed that detail around the time ProPublica approached Polis about his taxes.

Unlike ordinary investors, Polis was able to claim millions in deductions for some of the costs of his money management, specifically his family office, which contributed to lowering his tax burden. Ironically, the investment apparatus that helped Polis avoid taxable income became a tax break.

ProPublica discussed the scenario, without naming Polis, with Bob Lord, tax counsel for the advocacy group Americans for Tax Fairness. He said the public appears to be essentially subsidizing Polis’ investing while getting little in return. With a typical business, he said, you get the tax break but also relatively quickly make taxable income.

The costs of a family office are “being taken even though the income may be way out in the future. It’s just a giveaway,” Lord said. “What is the public getting from it? This really, really rich politician gets to shelter his income while his investments grow and doesn’t pay tax on it until he sells.”

Deferring paying taxes is a valuable perk. But the strategy, Lord said, may allow Polis an even more lucrative outcome. Now that Polis has made his fortune, he may be able to largely dodge the tax system forever. Should he die before selling his investments, his heirs would never owe income taxes on the growth.

Graham acknowledged that the tax system unfairly benefits the wealthy but said Polis is not purposely avoiding income that would result in taxes.

“The Governor has long championed tax reforms precisely because the income tax is inadequate and a mismatched way to tax most wealthy people who do not have a regular income but who make money in other ways and should be taxed,” she said. “Since 2006, Governor Polis has paid over $20 million in taxes on the money he earned on his gains and he has championed tax reforms that would lower the tax burden on middle-income earners and eliminate loopholes to ensure higher earners pay their share.”

ProPublica’s data shows that at least two federal officials have already taken steps to preserve their family fortunes for their heirs, exploiting loopholes that divert revenue from the federal government.

Scott, the Florida senator who ran one of the world’s largest health care companies, and DeVos, Trump’s education secretary and believed to be the richest member of his cabinet, have both stored assets in grantor retained annuity trusts — a form of trust used to avoid gift and estate taxes.

GRATs, as they’re commonly known, were accidentally created by Congress in 1990. Lawmakers were trying to close another estate tax loophole and in doing so unintentionally paved the way for another one. The lawyer who pioneered the trusts estimated in 2013 that they had cost the federal government about $100 billion over the prior 13 years.

To use this tax-avoidance technique, you put an asset, like stocks or real estate, into a trust assigned to your heirs. The trust pays you back the starting value of the asset (plus some interest). If the original asset rises in value, the gains can go to your heirs tax-free.

GRATs have become widely used among the superrich. A ProPublica investigation found that more than half of the nation’s richest individuals have employed them and other trusts to avoid estate taxes.

It’s unclear from ProPublica’s data how much DeVos, 63, and Scott, 68, were able to transfer tax-free.

DeVos and her husband employed a GRAT from at least 2000 to 2003. DeVos’ father was a wealthy industrialist. Her husband was the president of Amway, a multilevel marketing company that focuses on health, beauty and home products. Her family is believed to be worth billions.

Her causes both before and during her time in government depended on tax dollars. As a donor and fundraiser for Republican causes, she pushed for charter schools and government subsidies to allow parents to send their kids to private schools. As education secretary, she pushed to send millions of federal dollars intended for public schools to private and religious schools instead.

Scott, one of the wealthiest senators, with a net worth likely in the hundreds of millions, used a GRAT for much longer, from at least 2001 through 2009. His tax data shows the assets in the trust — stakes of a private investment fund and family partnership he and his wife created — receiving millions in income.

When he was in the private sector, Scott benefited from federal programs like Medicare, which are funded by taxes. He built and ran Columbia/HCA, a massive chain of for-profit hospitals. After a fraud investigation became public, he resigned and the company paid $1.7 billion to settle allegations it overbilled government health programs. Scott has previously emphasized that he was never charged, though he acknowledged the company made mistakes.

Scott declined to comment. Nick Wasmiller, a spokesman for DeVos, said she “pays her taxes in full as required by law. Your ‘reporting’ is not only factually wrong but also doubles-down on the criminal actions that underpin ProPublica’s political campaign to prop up the Biden Administration’s failing agenda.”

California Congressman Darrell Issa was one of a handful of Republicans who bucked his party in 2017 and voted against Trump’s tax overhaul.

Issa said he opposed the legislation because it all but eliminated the deduction taxpayers could take on their federal returns for state and local taxes. That provision was particularly contentious in high tax blue states like California, but most Republicans from his state still fell in line. The other GOP congressman in the San Diego area, for example, voted yes.

Limiting the write-off, known as the SALT deduction, was one of the few progressive changes in the Trump tax law. The deduction had long disproportionately benefited the wealthiest because they pay the most in state and local taxes. According to one projection, if the cap were removed from the deduction, households with income in the top 1% would reap the most benefit, paying $31,000 less a year on average — amounting to more than half of the total taxes avoided through the write-off. The top 25% of households would average less than $3,000 in savings a year, and the savings drop precipitously from there, with most households deriving no benefit.

In interviews and public statements, Issa said in fighting to preserve the deduction, he was defending the interests of middle-class taxpayers. “I didn’t come to Washington to raise taxes on my constituents,” he said at the time, “and I do not plan to start today.”

It’s true that more than 40% of taxpayers in Issa’s former district, a relatively affluent swath of Southern California, were able to make at least some use of the deduction.

But the 68-year-old congressman, who made a fortune in the car alarm business, was in the top echelon of its beneficiaries. Between 2003 and 2017, his tax data shows, Issa generally paid a relatively high tax rate but was able to claim more than $51 million in write-offs thanks to the SALT deduction, an average of more than $3 million a year.

By contrast, households in his district that made between $100,000 and $200,000 and took the SALT deduction claimed an average of $14,843 in 2017.

Issa’s spokesman, Jonathan Wilcox, declined to say if the SALT deduction’s impact on the congressman’s taxes factored into his decision to advocate for it.

“So much stupid,” Wilcox said. “Be sure to write back if you ever do better than trolling for garbage.”

Gov. Jim Justice is believed to be the richest person in West Virginia, controlling vast reserves of valuable steelmaking coal and owning The Greenbrier luxury resort. He made an appearance in 2014 on the Forbes list of 400 wealthiest Americans. Estimates of his net worth have ranged from the hundreds of millions to well over a billion.

Nonetheless, he’s paid little or no federal income taxes for almost every year between 2000 and 2018, ProPublica’s trove of tax records shows. In 12 of those years he paid nothing, and in all but two of those years, his rate didn’t exceed 4%.

His largest tax payment came in 2009, when his family sold off much of its mining holdings to a Russian company for more than half a billion dollars. That year, after deductions, his tax rate rose to a modest 13.4%.

In more recent years, Justice, 70, has reported tens of millions in losses each year. That not only helped him to minimize his federal income taxes, it also allowed him to apply those losses to his profits from previous years — and get refunds for the taxes he initially paid in those years.

Justice’s income was low enough in 2018 for his family to qualify for and receive a $2,400 coronavirus stimulus check, aid meant for low- and middle-income Americans.

The recent years of large losses reported on Justice’s tax returns have coincided with real signs of financial problems. The coal industry’s fortunes have rapidly declined. He’s been hounded for unpaid bills and loans. The Russian company that bought much of his coal empire sued him and got him to buy back the assets — at a much discounted price but attached to significant debt. Forbes knocked him off its wealth ranking, citing escalating battles with two major lenders over unpaid debt. Justice’s representatives have said he pays what he owes, and his business empire is in good shape.

But even before his empire began showing significant cracks, Justice was reporting losses or little income for a man so wealthy. From 1996 to 2008, Justice, who received a coal and farming fortune from his father, who died in 1993, either reported losses to the IRS or just a few hundred thousand dollars in income.

The disconnect could be explained by the generous deductions afforded to coal business owners.

For example, owners are allowed a depletion deduction, which allows them to take 10% of the revenue from coal they extract and write it off against their profit. This spin on depreciation can have outsized benefits because unlike normal depreciation — in which the write-offs are based on how much you paid for an asset — the write-off amount here faces no such limit, and can therefore exceed the initial investment. The deduction has been criticized by environmentalists and congressional Democrats as an overly generous giveaway.

Another benefit coal owners get is the ability to immediately expense much of their mine development costs on their taxes instead of being forced to stretch such deductions over a longer period of time. Justice has said that in the 15 years after his father’s death, he oversaw “a massive expansion of multiple businesses which included significant coal reserve expansion” — development that could have provided him with a significant stockpile of such write-offs. (ProPublica has previously reported on other generous write-offs. Sports team owners, for example, are allowed to deduct the value of their intangible assets — such as media deals and franchise rights — as wasting assets, even as they rise in value.)

Experts said this could explain how Justice could have reported negative income of $15 million in 2008, a year in which Mechel, the Russian company that subsequently bought much of his family’s coal empire, said that business alone produced about $94 million in EBITDA — a common measure of a business’ profitability before taxes and some other expenses.

Justice declined to answer a list of specific questions about his taxes. In a statement, his lawyer, Steve Ruby, said Justice “has paid millions upon millions of dollars in state and federal income taxes and has always followed the law. In many years, his businesses have suffered losses as the result of weak coal prices combined with substantial outlays to save jobs at local businesses that other companies were abandoning.

“When many other coal producers were filing for bankruptcy, the Justice companies persevered and refused to take the easy way out through a bankruptcy proceeding, a decision that contributed to those losses. Like any other taxpayer, Gov. Justice does not owe income taxes in years in which his income is negative,” the statement read.

Ruby confirmed that Justice received coronavirus stimulus checks but said he did not cash them.

Like Scott and DeVos, Justice has used GRATs to sidestep estate and gift taxes, his returns and court records suggest.

In 2008, the year before he sold much of his coal empire to the Russian company, two GRATs appeared on his returns for the first time. And when the Russian company sued Justice, it also sued him in his capacity as the trustee for those GRATs. Justice had placed at least some of the coal assets into the trusts before the sale, according to the lawsuit.

Ruby’s statement did not address Justice’s use of GRATs.

Ask almost any billionaire how they got so obscenely rich and , invariably, you will get the response: “I just did what the law allows” or some convoluted version of that idea. Tax laws, property and financial regulations and structures, corporate stock options, Roth IRA tricks, all the tried and true methods outlined in a slate of recent articles from ProPublica and others are rightfully given credit for the insanely massive windfalls.

Not that these arrogant, self-centered sociopaths don’t jump at the chance to take credit for their “miraculous” good fortune, or even write books and “let” others write books about all the “genius” ideas and methods they used to conquer the universe.

Jeff Bezos is the most ridiculous example of this, literally dozens of books exist only to extol the virtues and genius of this a-hole that basically used one simple trick: selling dollar bills for .75 cents and using the stock market to “monetize” a trillion in intentional losses and turn them into “wealth”, to amass his absurd mountain of “worth”, yet if you read these books the central concept of his fraud doesn’t even get a mention.

Of course, 25 years later, the FTC and Lina Khan are finally beginning to wake up to the simple fact that, not only is the entire scam something that “ought-a-be-illegal”, but literally is illegal and always was, yet this comes across, so far, as a somewhat pathetic attempt to put a band-aid on the world after a nuclear holocaust has already devastated the planet.

When we say “tax the rich,” we mean nesting-doll yacht rich. For-profit prison rich. Betsy DeVos, student-loan-shark rich.

AOC used her beauty and a cheeky dress to highlight the issue of income inequality

Above: Photo / Wikipedia

AOC at the Met Gala styled herself in a “Tax the Rich” gown. The look on her was beautiful. The subject matter being broached couldn’t be uglier. Tax the rich a not a bad idea, but the system is so screwed up, and so far from any semblance of “fair”, that a few little pin pricks on trillions in undeserved holdings is basically meaningless.

How can it be said that the system is that far gone? It’s in the numbers and the proportions of “wealth”. The extremes of unequal wealth distribution have risen to levels so incredible, that it’s as if they are turning into an economic ouroboros dragon that will expand and swallow itself until it has devoured all life.

The increases, during the pandemic, for example, in the “net-worth” (which is in itself an obscene concept for measuring humans) of the worlds richest animals was like the replication of the virus the rest of us were fighting to avoid, most with too few resources to have any hope of being rescued by medical intervention, if we got infected.

This idea and proof of a system vastly out of balance can be seen everywhere you look…

In a recent, excellent, NYT article on Afghanistan multiple examples were cited illustrating who really “won” that endless war, and points out that it wasn’t the just Taliban. It was locals entrepreneurs and politicians who, early on, saw the opportunity for what it really was, a way to build personal fortunes supplying the US military with support and comfort during the endless, directionless morass.

Several examples were of people who began the war as local american sympathizers and ended up with fortunes hundreds of millions of USD and more, virtually none of which trickled into the local populations which, ostensibly, the war was meant to give a chance for “democratic freedom”. And capitalism.

Here’s a couple of paragraphs from the NYT article in full :

”Consider the case of Hikmatullah Shadman, who was just a teenager when American Special Forces rolled into Kandahar on the heels of Sept. 11. They hired him as an interpreter, paying him up to $1,500 a month — 20 times the salary of a local police officer, according to a profile of him in The New Yorker. By his late 20s, he owned a trucking company that supplied U.S. military bases, earning him more than $160 million.”

“If a small fry like Shadman could get so rich off the war on terror, imagine how much Gul Agha Sherzai, a big-time warlord-turned-governor, has raked in since he helped the C.I.A. run the Taliban out of town. His large extended family supplied everything from gravel to furniture to the military base in Kandahar. His brother controlled the airport. Nobody knows how much he is worth, but it is clearly hundreds of millions — enough for him to talk about a $40,000 shopping spree in Germany as if he were spending pocket change”